You have heard it pays to shop around for homeowners’ insurance rates but price is only part of the equation. NBC 5 Responds Consumer team talks about ways to make shopping for insurance easier,

You’ve heard it pays to shop around for homeowners insurance rates, but price is only part of the equation. Policies vary depending on coverage limits, deductibles and exclusions.

Here are some key questions to ask when you shop for insurance.

‘PROBABLY TOO SCARED TO SWITCH’

On a recent sunny summer day, NBC 5 Responds asked consumers to talk about a hot topic: the cost of homeowners insurance.

Get top local stories in DFW delivered to you every morning. Sign up for NBC DFW's News Headlines newsletter.

“Everything's expensive,” said Pamela Kinney of Greenville, Texas. “Everything's pricey.”

Another homeowner, Keith Grissom of McKinney, said he hasn’t comparison-shopped in a while.

“Not lately at all,” Grissom responded.

“Just did it last month,” said Susie of Rockwall.

Vickie Moore, also of Greenville, said she’s been in the same insurance company for more than 20 years.

“Why do you think you've been with the same insurance company so long?” NBC 5 Responds Reporter Diana Zoga asked.

“Probably too scared to switch,” said Moore.

COMPARING ‘APPLES TO APPLES’

The stakes are high for consumers, trying to protect their biggest asset, while costs rise.

“Unfortunately, consumers have to be a little more proactive in that process than they used to be,” said Emily Rogan with the nonprofit United Policyholders.

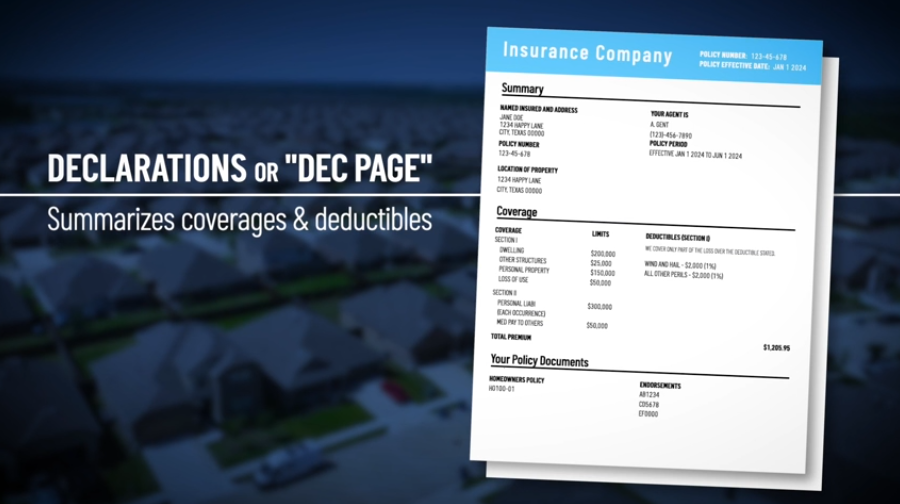

Rogan said consumers should dig out their current policy. The first page or two, the declarations or dec page, summarizes coverages and deductibles.

“The most important thing is that you're shopping apples to apples,” Rogan said. “Make sure the amount for your coverage, which is your dwelling, is, first of all, enough to rebuild your home. When you're shopping around, make sure that number stays the same so you know you're getting a fair comparison.”

When comparing deductibles, the out-of-pocket cost you’d pay for each claim, confirm if it changes depending on the type of loss. For example, the same policy may carry a one or two-percent deductible for many losses and a six-percent deductible for hail or wind damage. How much would you pay for different claims like hail, fire or theft? Do the math to find out how much you’d pay out-of-pocket for each potential risk. Or, ask your insurance provider.

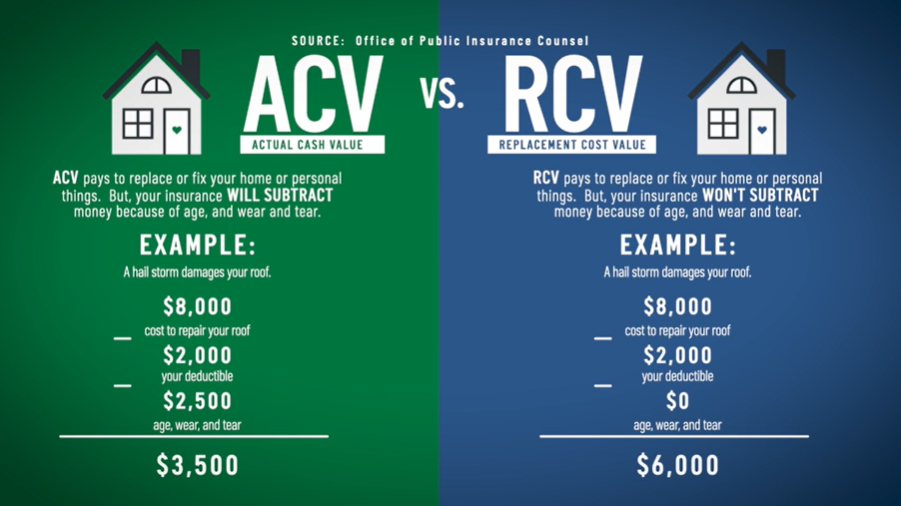

Look for terms like actual cash value (ACV) or replacement cost value (RCV). As the Office of Public Insurance Counsel explains ACV coverage pays less than RCV coverage because it factors in age and wear and tear. Confirm if you’d have replacement cost value coverage for all covered items. Or, if some property is paid at actual cost value.

While the “dec page” is a good starting point to understand your insurance coverage, Rogan recommends reading any policy fully.

“Even if your coverage is right, maybe you have a sewer backup limit that is very low,” explained Rogan.

SHOPPING FOR DISCOUNTS

There may be discounts for members of the military. You may shop for potential discounts through your employer or alumni group. If you’re combining policies, like auto and home, shop them separately to confirm a bundle is a deal.

Consumers can ask insurance providers about discounts related to home improvements, like extra security measures.

“Some of them offer technology packages. They'll send you a couple of water detection devices, maybe a camera doorbell,” said Rich Johnson, with the Insurance Council of Texas, a trade group representing many insurers in Texas.

Johnson said each insurer assesses risk their own way. It may identify a risk in drone or aerial images of your home.

“There's a lot of folks I know, even in my neighborhood, their kids are grown, but they still have that trampoline laying around. That's going to show up in aerial imagery of their home,” Johnson said. “Sometimes you'll actually be denied coverage completely if you have the wrong kind of trampoline or a trampoline at all.”

Rogan with United Policyholders said to try to confirm the images your provider used are current and correct. If you’ve addressed an issue, let them know.

“Ask your insurance company,” said Rogan. “If they are saying you have junk in your yard, there is a nuisance in your yard, make sure that you ask them for the photos. They might not give them to you, but you can have that conversation.”

If you buy a new policy, cancel your old one and request a refund of the unused premium. Make sure the insurance change is communicated to your mortgage lender.

Homeowners can switch policies anytime – even outside a renewal period.

‘GET MORE THAN JUST ONE OPINION’

“Have somebody that knows what they're talking about. They can explain to you what each coverage means,” Kinney said.

“Get more than just one opinion,” Moore agreed.

Keith Grissom said customer service keeps him with the same insurance provider.

“Even if it's a little less or a little more, I’m okay with that if they treat us well and like we matter,” said Grissom.

Susie from Rockwall said she’s committed to collecting quotes for the best available price.

“I want to be honorable with the blessings that God has given me,” Susie said.

Zoga responded, “So, you’re going to shop around?”

“Always,” said Susie. “Everything in my life I will always try to get the very best. The more you save, the more you can give.”

RESOURCES TO HELP YOU RESEARCH

The state has a comparison tool at www.helpinsure.com It asks you questions about your property location, claim history, credit score and the estimated cost to rebuild your home. It searches sample policies along with company ratings. You’d still have to contact the specific insurance provider to get an exact quote.

Consumers can also review claims reported about their property or vehicle. The Comprehensive Loss Underwriting Exchange or C.L.U.E report lists claims filed for a house or car for the past seven years. Experts told NBC 5 Responds, that consumers should ensure their reports are accurate or they risk paying more for insurance. You can request a copy, for free, every year. A consumer’s claims history may also be in an A-PLUS loss history report run by the Verisk database.

Insurance companies may factor in a consumer’s credit score when deciding rates or whether to sell coverage to a consumer. Consumers should check their credit reports, regularly. You can find out more about checking your credit report for free here. The major credit bureaus now allow consumers to review their credit reports for free every week. Pre-pandemic, consumers could access the information at no charge annually.

The TDI publishes a home insurance consumer guide here. A consumer may shop with insurance company agents, independent agents and brokers. Or, a consumer may buy insurance directly through an insurance company website or by phone. Consumers should understand a typical homeowners policy wouldn’t cover flooding.

Consumers would have to purchase separate insurance, typically from the National Flood Insurance Program, administered by FEMA. Mortgage lenders may require flood insurance in some places. However, flash flooding could happen anywhere. On average, FEMA says around 40% of NFIP claims come from outside high-risk flood zones. You can find out more about finding flood insurance coverage here.

NBC 5 Responds is committed to researching your concerns and recovering your money. Our goal is to get you answers and, if possible, solutions and a resolution. Call us at 844-5RESPND (844-573-7763) or fill out our customer complaint form.

Get top local stories in DFW delivered to you every morning. Sign up for NBC DFW's News Headlines newsletter.