How much do you think you need to retire comfortably? NBC 5’s Alanna Quillen tells us about the new details.

Cooling inflation and a solid job market have brought a sign of hope for your wallet this week.

The Federal Reserve Chair Jerome Powell announced that the central bank plans to make cuts to the interest rates sooner rather than later.

Speaking at the Economic Club of Washington D.C., Powell referenced the idea that central bank policy works with “long and variable lags” to explain why the Fed wouldn’t wait for its target to be hit.

“The implication of that is that if you wait until inflation gets all the way down to 2%, you’ve probably waited too long, because the tightening that you’re doing, or the level of tightness that you have, is still having effects which will probably drive inflation below 2%,” Powell said.

Get top local stories in DFW delivered to you every morning. Sign up for NBC DFW's News Headlines newsletter.

He did not say exactly when the Fed might start to cut rates. Their next policy meeting is at the end of July.

Interest rate cuts are welcome news for those wanting to buy a home. However, a new study shows many millennials might not even have the savings to do that – and even worse, many are nowhere near where they should be in retirement savings.

On average, Americans say they'll need around $1.46 million saved up to retire comfortably, according to Northwestern Mutual's "2024 Planning and Progress" study. And for millennials, the majority of whom are in their 30s, that number is a little over $1.6 million.

Local

The latest news from around North Texas.

However, many in their 30s are far from reaching that goal right now.

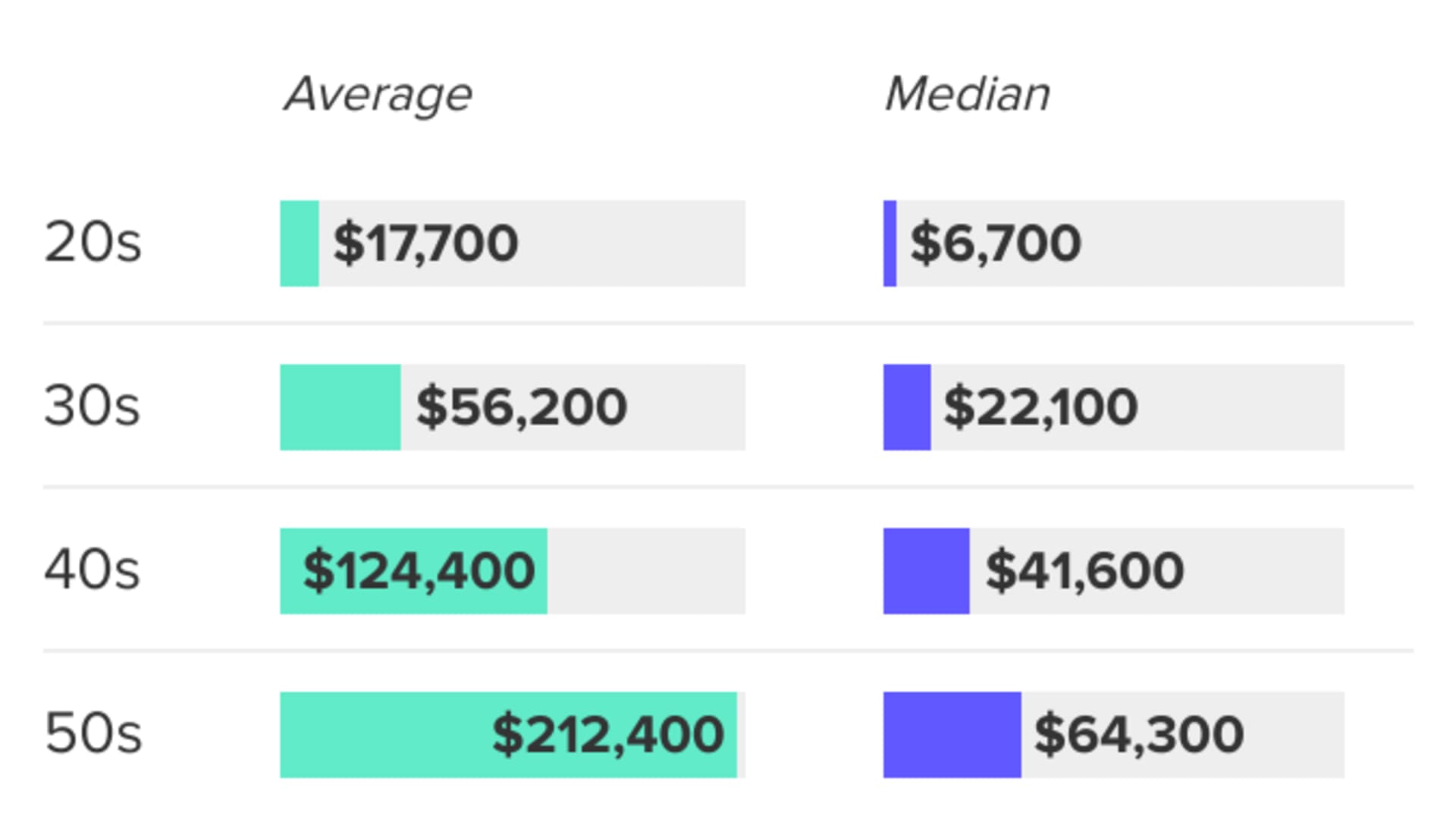

The median 401(k) balance for people in their 30s is around $22,100 as of the first quarter of 2024, per the latest data from Fidelity Investments, one of the country's largest 401(k) providers.

Here's how much Americans have in their 401(k)s by age, according to Fidelity:

"I think in almost all age brackets, they're only about a quarter of a percent of where they should be, right? Which is kind of eye-opening,” said Josh Perkins, vice president at DeWitt & Dunn Financial Services in Dallas. “But right now, obviously with inflation and everything, it's kind of difficult for people to put more money aside.”

Data in the study further shows that nearly half of Americans say they don’t even have a dedicated retirement savings account, like a 401(k) or IRA.

It varies by age, those who are just starting out saving for retirement may not have much in their savings.

- 49% under 35 have $18,880

- 61.5% between 35-44 have $45,000

- 62% between 44-54 have $115,000

- 51% between 65-74 have $200,000

Among the causes for the struggle to save money, experts point to inflation-tightening wallets in the last three years. The post-pandemic difficulties in the economy have also led to a record amount of credit card debt across the country, which is affecting how much extra money people can put towards their savings. Retirement has become an afterthought for many.

"I don't know if you've heard of the phrase 'money dysmorphia' – where a lot of Gen Z and millennials are having the ‘Keeping up with the Jones’ syndrome. They're inundated through social media of always seeing everybody's best life – wonderful trips that people are taking, new cars and houses people are buying,” said Perkins "And they think that they need to be able to somehow afford that. So they go into more debt than they should. I think that's just a combination of inflation and people not really planning for the future."

The way generations approach saving is also different. Boomers began saving for retirement at 37, while Millennials began at 27 and Gen X at 31.

Younger generations are expecting to retire earlier, which means they will need their money to last longer. Gen Z wants to retire at 60, a full 12 years earlier than Boomers.

REACHING RETIREMENT GOALS

"When it comes to saving for retirement, 10 years ago was always the best time to start. But if you haven't started yet, then the second-best time to start is going to be today,” said Perkins.

For 2024, individuals can contribute up to $23,000 to a 401(k) plan.

Unfortunately, one in four couples say they are not taking advantage of matching company contributions being offered for their employer-sponsored 401(k) plan.

Perkins recommends contributing 10% to 15% of every paycheck to your 401(k). If you can’t manage that, you need to be contributing at least enough to get the company to match.

Automating contributions directly from the paycheck into your 401(k) or other retirement accounts will make it less tempting to spend the money rather than save it.

You can also automate the increases at which the contributions occur over time. Experts say you should consider contributing an additional 1-2% annually or every six months.

"I think the first step would be understanding how much money you have coming in. Once you're able to control your spending and your personal finances, then you can start planning for the future with the leftover money, staying out of debt, and keeping your credit card debt low or no credit card debt at all,” said Perkins.

DON’T FORGET ABOUT TAXES

Even though we all pay taxes every year, only 30% of Americans have a plan to minimize the taxes on their retirement savings.

Just putting money into a 401(k) may not be enough if their plan doesn’t take into account the impact of taxes on their retirement income. When you withdraw from your accounts in retirement, you could be taxed between 20 to 30%.

Perkins says to minimize taxes, you can make a charitable donation from a taxable account that is tax-deductible or use a Health Savings Account (HSA) to pay for medical expenses. Withdrawals for qualified expenses are tax-free.

OPEN AN IRA

Consider opening an individual retirement account (IRA) for additional income in retirement.

There are two main types of IRAs: Traditional and Roth. Contributions to a traditional IRA are tax deductible and the investment earnings can grow tax-deferred until you withdraw the funds in retirement.

With Roth IRAs, your contributions are taxed upfront, grow tax-free and you are able to withdraw the money tax-free in retirement.

LEVERAGE CATCH-UP CONTRIBUTIONS

Retirement accounts are designed to help workers age 50 and older by allowing additional catch-up contributions.

In 2024, the catch-up contributions for those workers is $7,500.

If you’re serious about retiring, save as much as you can while you’re still earning a paycheck.

For more tips on retirement, click here.